Business Owners

Whether you are a sole trader or owner of a large company, and regardless of whether you enjoy every minute of your working life or you are counting down to the days to when you plan on stepping back from your business, it makes sense to plan for your future in a tax efficient manner.

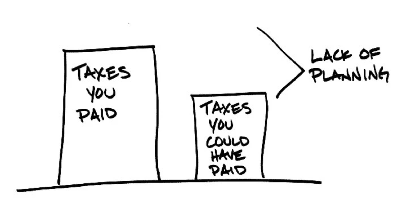

Nothing is certain except death and taxes as Benjamin Frankin once famously said but with careful financial planning you may be able to minimise those taxes.

Everyone’s personal circumstances are unique and there are many considerations as to what your preferred course of action might be when it comes to extracting cash from your business in a tax efficient manner.

Typically, through one of (or a of combination of), the following measures you may be able to minimise your liabilities to Revenue when it comes to extracting wealth from your business in a tax efficient manner;

- Retirement Relief, whereby you can earn up to €750,000 tax free from the sale of your business completely tax free;

- Entrepreneur Relief, where you can avail of a reduced rate of Capital Gains Tax of 10% (versus 33% typically) on the sale of your business;

- Share Buy-Backs whereby gains can be subject to Capital Gains Tax as opposed to your marginal income tax rate (often 52% or more) and/or;

- Maximum pension funding up to €2,150,000, whereby the first €200,000 of any pension lump sum is entirely tax free, and the next €300,000 subject to income tax at the lower rate of 20%.

Each of the options listed above, which is not an exhaustive list of possible tax efficient wealth extraction options, have their own set of stringent standalone criteria which must be satisfied before you can qualify for that tax efficient wealth extraction option.

By way of example, to qualify for Retirement Relief, you must at time of writing hold either a) 25% of the voting rights of your company or, b) 10% of the voting rights and, together with your family, hold at least 75% of the voting rights, for a minimum of 10 years before any sale.

The €750,000 tax free amount mentioned above is a lifetime limit and while you may well easily satisfy this element of the criteria, does your spouse satisfy this criteria also? If not, and if your company is likely to sell for in excess of €750,000 at some point in the future, you may be creating a tax liability for you and your family that could easily have been avoided with some careful financial planning in well in advance.

Regardless of your circumstances, the point to note is that it’s never too early, or is it ever too late, to start having conversations about your future. There’s a popular Chinese proverb that says: “The best time to plant a tree was 20 years ago. The second best time is now!”

How Do You Increase The Value Of Your Business Before You Sell?

It’s a question that all business owners want to know the answer to. There are lots of steps that you should consider taking to maximise the sale proceeds of your business which I allude to further on in this article but first I think it timely to recount the parable of The Mexican Fisherman And The Investment Banker.

‘An American investment banker was taking a much-needed vacation in a small coastal Mexican village when a small boat with just one fisherman docked. The boat had several large, fresh fish in it. The investment banker was impressed by the quality of the fish and asked the Mexican how long it took to catch them.

The Mexican replied, “Only a little while.” The banker then asked why he didn’t stay out longer and catch more fish? The Mexican fisherman replied he had enough to support his family’s immediate needs. The American then asked “But what do you do with the rest of your time?” The Mexican fisherman replied, “I sleep late, fish a little, play with my children, take siesta with my wife, stroll into the village each evening where I sip wine and play guitar with my amigos: I have a full and busy life, señor.”

The investment banker scoffed, “I am an Ivy League MBA, and I could help you. You could spend more time fishing and with the proceeds buy a bigger boat, and with the proceeds from the bigger boat you could buy several boats until eventually you would have a whole fleet of fishing boats. Instead of selling your catch to the middleman you could sell directly to the processor, eventually opening your own cannery. You could control the product, processing and distribution.” Then he added, “Of course, you would need to leave this small coastal fishing village and move to Mexico City where you would run your growing enterprise.”

The Mexican fisherman asked, “But señor, how long will this all take?” To which the American replied, “15-20 years.” “But what then?” asked the Mexican. The American laughed and said, “That’s the best part. When the time is right you would announce an IPO and sell your company stock to the public and become very rich. You could make millions.” “Millions, señor? Then what?”. To which the investment banker replied, “Then you would retire. You could move to a small coastal fishing village where you would sleep late, fish a little, play with your kids, take siesta with your wife, stroll to the village in the evenings where you could sip wine and play your guitar with your amigos.’

The above parable brings clarity to what money is all about… and what it’s definitely not about. It brilliantly illustrates the illusions we so easily fall into when pursuing wealth and financial freedom. It’s far too easy to build incessantly and forget the end game is happiness and a fulfilling life. Human nature being what it is you will want to get the biggest possible number for your business however too may entrepreneurs confuse “the biggest number possible” with what is actually important… “how much they actually need to achieve all their desired goals in life from that point forward”.

Knowledge is power the point of the above parable is that knowing exactly how much you need for the remainder of your days is far more valuable when negotiating a sale price than actually knowing what the maximum amount is that you can get for your business. Sure, you’re not going to accept a disrespectful offer for your business however if that figure was more than enough to live out your ways the way that you wanted, would you agree that perhaps that offer might be worth another look?

A similar (and true) story to that of the Mexican Fisherman above is that of a business man who owned a successful business but the time had come where he wanted to sell. He had an offer on the table of €2.5m but was reluctant to sell on the basis that his accountant had assured him that his business was worth €3.5m “all day long”. The business owner met with his Certified Financial Planner™ and, by aligning the business owners long term personal goals in life with prudent assumptions in terms of future investment returns and the cost of achieving all his goals, the business owner accepted the €2.5m offer, comfortable in the knowledge that he was highly unlikely to ever outlive his money. The year was 2008. After the sale, the value of his former company fell to €1.5m and took approximately 8 years to return to the €2.5m value that he had achieved in 2008. The former business owner had successfully avoided a situation whereby he would have essentially worked 8 additional years for free! Nobody likes working for free…

Selling Your Business

The day is approaching fast. You’ve worked hard, you’re reaching the summit of your career and you are about to reach a critical juncture in your life; you want to sell your business. It can be an exciting time full of opportunity but it very often can also be a stressful time. You have concerns that the sale price might not be enough to sustain you or your family for the remainder of your life, you have concerns that the sale might not be completed in the most tax efficient manner possible, you may even have concerns that this business, which you have developed over a number of years, is so intrinsic to your identity that once sold, you may even feel a certain sense of loss.

We have identify below 5 primary reasons why businesses fail to sell, and you can do today to increase the likelihood of a achieving successful sale of your business…

1. Poor documentation and records

Whilst you are no doubt excellent at what you do, ‘paperwork’ may not be your area of expertise. Your accountant has guided you to this point and kept you on the straight on narrow however it has come to the point that an interested 3rd party now wants to take a deep dive into your and your business. On the surface everything looks to be running smoothly but under the hood you know that they’re an engine running that you are fully in control of.

If sometime goes wrong, you know how to fix it which is great, but you need to go a step further. Who fixes it when you’re no longer there? This is a major concern for any prospective buyer but it’s one that you can allay by performing the following tasks in the years leading up to any potential sale;

- Have your audited accounts submitted each year on time, every time;

- Ensure that all tax returns are up to date and that there has been no reason for Revenue to contact you in the past few years regarding late tax filings;

- “Turnover for show, margin for dough”. Focus on your margins. The last thing any perspective buyer wants is to buy a company that increases their workload but dilutes their gross and net profit margins.

- Take control of your working capital; Ensure all trade debts are being collected in a timely fashion and well within credit control periods. Weed out “problem clients”.

- Prepare you own ‘Due Diligence Document’. Ask yourself, “if you were purchasing a company like yours, what are the key questions that you would like to know the answer to before committing to purchase?”. This could include everything from the history of the business to details on the current staff members, to a full SWAT (Strengths, Weaknesses, Opportunities and Threats) Analysis.

- Prepare a “Policies and Procedures Manual”/Operating Manual in as much detail as you can, outlining “if this, then that”, for all aspects of your business.

2. The valuation gap

A question that you likely regularly moot over is “how much is my business worth?”. In reality, and as alluded to above, a far more important question is “how much do I need to live out the remainder of my life the way I want to live out the remainder of my life?”.

What are you biggest ambitions in life? What do you want your legacy to be? These should be the first questions that you should be asking yourself at this point in time. These are not easy questions to answer but they can be answered. And once you know the answers to these questions you can, in conjunction with your Certified Financial Planner™ identify a minimum sale figure for your business, allowing you go enter into any negotiation armed with the key information that you need to make an informed decision about the potential sale of you business.

3. Market outlook

As you will be aware, from time-to-time unforeseen events beyond our control can and do change the course of business. Never has this been more evident than in the recent past where we experienced, and continue to experience, the negative effects of Brexit and the Covid-19 pandemic. You won’t ever be able to control what happens on a macro-economic level but you can, to a large extent, control the timing of any sale. If your business is cashflow positive but the market for sale isn’t in your favour, it may be prudent to continue to operate as normal and to use that time to get your affairs in order. If you are intent on stepping back from the day to day running of the business it may be an optimum time to make a key hire within

your business, allowing you more time to work on your business as opposed to in your business, readying the business for a potential future sale.

4. Holding on for too long

Life is full of ifs, buts and maybes but sooner or later you’re going to have to call it. And you’re going to have to live with that decision. It may scare you to walk away from the business that you nurtured from the early days to what it is today but that’s not a reason to stay longer than you need to. Life is not a rehearsal. When you know your number (see point 2 above), you’ll soon realise that there’s more to life than the 80 hour weeks that you had been doing in your business to get it to where it is today.

“Perhaps my best years are gone. When there was a chance of happiness. But I wouldn’t want them back. Not with the fire in me now. No, I wouldn’t want them back” – Samuel Beckett, Krapp’s Last Tape & Embers

Determine what your next act will be. It’s time to show the world that there’s more to you than the business where you’ve spent the supposedly “best years of your life”.

5. No succession planning

You value you family. You value your family so much that the thoughts of having an awkward conversation with any of them at this time about their future intentions and the possibility of them not wanting (or wanting!) to take over your business scares you. The conversation gets put on the long finger again and again to the point that the opportunity to have the conversation slips by. The dye is cast almost by accident than design and with that, the possibility of a smooth transition of your business to the next generation.

Very often the only thing worse than a bad decision is indecision. The importance of expressing your long term intentions to your family can’t be over emphasised. You may be pleasantly surprised as to how your family/the next generation might respond to your plans. You may also be disappointed to learn of their plans yet once you know what an exit for you from your business might ultimately look like, you can plan accordingly. Knowing this

information will be important from a tax planning point of view. Don’t delay this conversation longer than you already have, for your own tax planning reasons if nothing else!

Food for thought

Regardless of your future plans to exit from your business, serious financial planning well in advance of any potential sale is a prerequisite for all business owners to ensure that the maximum number of possible exit options are kept on the table so that when you do decide ultimately to sell your business, you can utilise an exit strategy that suits you and your circumstances best at that time. Without careful financial planning in advance, you may inadvertently limit your exit options, and possibly inadvertently incur what could otherwise have been an easily avoidable tax liability for you and your family.