When you picture your retirement, you likely imagine maintaining your current lifestyle and enjoying the freedom you have worked hard to achieve. However, recent data paints a concerning picture for Irish professionals and business owners.

A pension replacement rate measures the percentage of your working income that you will keep once you retire. According to the latest OECD figures, the net replacement rate for an average earner in Ireland sits at just 33.7%. This represents a steep and immediate drop in disposable income. Understanding this gap is the very first step toward securing your financial independence.

The European Contrast and The High Earner Penalty

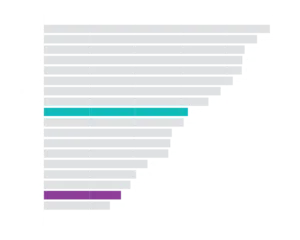

When you look at the wider European map, the contrast is stark. CCountries like Portugal boast a replacement rate of 98.8%, with the Netherlands securing 93.2% of a worker’s income and Luxembourg reaching 87.7%. Meanwhile, Ireland sits near the bottom of the table at 33.7%, far below the overall OECD average of 63.0%.

Our system is fundamentally different from those of our continental neighbours. The Irish public pension is a basic scheme paying a flat rate to all who meet the contribution conditions. Currently, the maximum State Pension (Contributory) provides €299.30 per week. While this serves as a vital safety net, it is absolutely not designed to replace the incomes of high earners, company directors, or business owners.

In fact, the OECD notes that the lowest replacement rates for high earners worldwide are found in Canada, Estonia, Ireland, Korea, Lithuania, New Zealand, and Switzerland. In these countries, workers earning 200% of the average will receive net pensions that amount to 25% or less of their net earnings when working. Consequently, high net worth individuals face the most significant income drop in percentage terms when they retire, making proactive private funding essential.

Navigating the Auto-Enrolment Era

To address the broader national coverage gap, the government introduced the Automatic Enrolment Retirement Savings System, known as “My Future Fund”, at the end of September 2025. This new framework operates on an opt-out basis, where employers match contributions on a one-for-one basis. Additionally, the State provides a top-up of €1 for every €3 saved by the employee.

While this initiative marks a positive shift for the general workforce, it is fundamentally inadequate for high earners. The scheme is strictly capped and designed solely to support average income levels. For business owners, company directors, and senior professionals accustomed to a higher standard of living, this basic structure simply will not generate the wealth required to bridge a massive retirement income gap. Relying on auto-enrolment means accepting a drastic reduction in your lifestyle, making bespoke private funding an absolute necessity.

How Chartered Capital Can Help

The evidence is clear. You cannot rely on European-style state pension security in Ireland. Instead, the responsibility for a comfortable retirement rests firmly on your shoulders, and this is where Chartered Capital steps in to help.

We specialise in building proactive, private financial strategies for high net worth individuals. By taking advantage of tailored tax reliefs, bespoke executive pension structures, and globally diversified investment portfolios, we help you build a robust safety net of your own.

Specifically, we analyse your current wealth, project your future needs, and create a structured roadmap that ignores the noise and focuses entirely on your long-term goals. The earlier we address your unique shortfall, the easier it becomes to smooth out your income journey from your working years into your retirement.

Final Thoughts

Ireland’s low pension replacement rate is a wake-up call, but it certainly does not dictate your future. By understanding the limitations of the State system, you can take decisive action today. You have the power to close the income gap and build lasting wealth with the right advisory team by your side. Book a confidential consultation with Chartered Capital to design a retirement strategy tailored to your retirement lifestyle goals.

The content of this article is for information purposes only and does not constitute a personal recommendation. You should always speak to a financial adviser that is regulated by the Central Bank of Ireland when considering financial advice. Any recommendation made will be based on a full suitability assessment that will include a comprehensive review of your circumstances, needs and objectives. Past Performance Is Not A Guide To Future Returns.

In Their Own Words